US Economy and Rates Update January 15, 2019

Key Highlights

- We were early last year to call for just two hikes in 2019, initially placing them in March and June.

- With “patience” returning to Fed policymakers’ communications due to recent financial market developments and emerging downside risks to the global economy, we believe the FOMC’s message is clear: policy is on hold for at least the next three months until the implications for real economic activity are discernible.

- While our base case of two hikes remains appropriate in our view, we are adjusting our expectations on the timing of those hikes. We now expect the FOMC to raise interest rates in June and December.

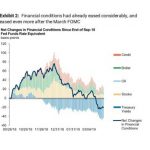

- In the interim, policymakers will continue their internal and external conversations on the Fed’s balance sheet normalization process and its impact from the perspectives of both technical policy implementation considerations and its effects on financial conditions.

US Rates Strategy

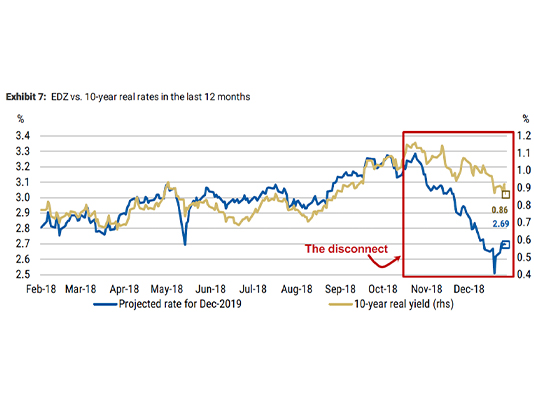

- We lower our below-consensus 2019 Treasury yield forecasts further. We now see the 10y Treasury yield ending 2019 at 2.45% (down from 2.75%, which was also our forecast for year-end 2018).

- We still forecast an inverted curve in 2019, given our economists’ projection of a rate hike in June and another in December. If the Fed is unable to deliver these hikes, the yield curve might not invert.

- The early end to balance sheet normalization we forecast should contribute to the curve inversion and to lower Treasury yields.

- With a patient Fed, we see real rates now moving lower through 2019, to levels last seen before fiscal stimulus was enacted in 2018. We see 10-year real rates ending 2019 at 55bp. We see 10-year breakevens recovering a bit, and ending 2019 at 190bp.

Recent Posts

{kind=link}