US Economy and Rates Update March 31, 2019

Key Highlights

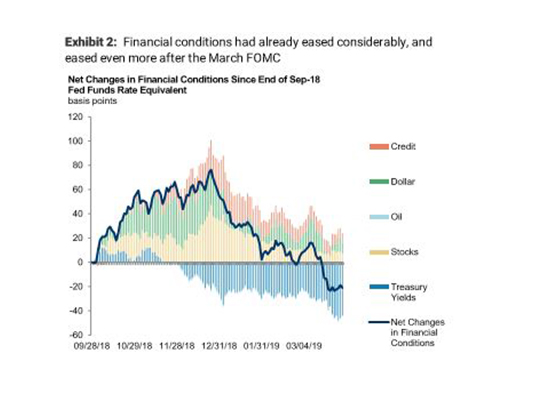

- The Fed’s move to a median of zero hikes this year was a surprise. Analysts and the markets underestimated Chair Powell’s appetite to deliver a preemptive strike against downside risks to the outlook. At the same time, the Committee has moved to wait-and-see mode, backing away from any hints about what further policy adjustments may be necessary down the road.

- Based on this more fluid reaction function, analysts have removed the December hike, leaving the Fed on the sidelines for the year. Having the Fed on the sidelines into next year lowers subjective probability of a recession starting in 2020 from 30% to 20%. The longer the Fed is on hold, the more slack is reduced and inflationary pressures build, drawing the Fed back into the hiking cycle in 2020.

- Oddly, the Fed’s dovish turn has helped drive the yield spread between the 3m T-bill and the on-the-run 10y Treasury note negative, inconsistent with economic fundamentals. We have to get past a noisy quarter that is shaping up to be quite sluggish, but more recent data, on balance, point to a rebound in 2Q. Market concerns about recessions can be self-fulfilling, however, and can sway the Fed for that reason.

- What if analysts are wrong and instead we are moving not through a trough in growth, but into a downturn? Expect Chair Powell to act decisively and aggressively, buying insurance against hitting the zero lower bound by cutting rates 50bp. Consider it another preemptive strike.

- Strategists now see the 10y Treasury note yield ending the year at 2.25%, down from 2.35% previously. Real rates do the heavy lifting as nominal yields decline on the forecasts. Analysts see real yields ending the year back around pre-tax reform levels – consistent with the fiscal impulse fading completely.

Recent Posts

{kind=link}